India’s IT sector is going through a phase that feels uncomfortable but not unfamiliar. After years of strong growth and premium valuations, the sector is now facing a sharp correction driven by changing global dynamics. Stocks of leaders like Infosys, TCS, HCL Tech, and Wipro have declined despite reporting fairly stable Q4 results. This divergence between earnings and stock price reflects one key reality that markets are forward-looking. The Nifty IT index has corrected close to 8-10% in a short span, showing how sharply sentiment has shifted even when headline numbers did not collapse.

Q4 Performance Still Holds Ground

The Q4 FY26 earnings season indicates that India’s IT sector delivered stable and resilient performance, even as stock prices corrected. The sell-off is not due to weak results but concerns around slower future growth.

Infosys reported revenue of ₹46,402 crore, growing about 13% YoY, while net profit rose over 20% to ~₹8,500 crore. Margins remained steady at around 21%, showing strong cost control.

TCS posted revenue of ₹70,698 crore with ~10% YoY growth, and net profit of ₹13,718 crore, up around 12% YoY. It maintained industry-leading margins of ~25%, reflecting strong operational efficiency.

HCL Tech reported revenue of ~₹33,900 crore with ~12% YoY growth, while profit stood near ₹4,400-4,500 crore. Margins remained stable in the 20-22% range, although deal momentum slowed slightly.

Wipro delivered revenue of ₹24,000+ crore, with margins improving to around 17%, indicating better efficiency despite modest growth.

Across the sector, operating margins stayed in the 20-25% range, highlighting that profitability remains intact. Companies also reported strong deal wins, with TCS clocking ~$12 billion in total contract value.

However, sequential growth remained muted, and deal conversions are slower due to cautious client spending and delayed decision-making.

Overall, Q4 results reflect stability, not weakness. The current correction is driven more by weak guidance and slowing growth expectations, rather than any deterioration in earnings.

Guidance Becomes the Real Trigger

The recent correction in IT stocks is primarily driven by weak forward guidance rather than Q4 performance. Infosys has projected revenue growth of around 1-3% for the upcoming year, a sharp decline from the 10-12% growth seen in earlier periods. Similarly, TCS has indicated that demand recovery will be gradual and uncertain, with no strong near-term momentum.

This slowdown in growth expectations directly impacts valuations, as stock prices are largely based on future earnings potential. When growth shifts from double digits to low single digits, premium valuations become difficult to justify. Even with stable margins and profits, lower growth reduces earnings visibility.

As a result, the market is re-rating IT stocks, adjusting valuations to reflect a slower and more realistic growth environment.

Demand Is Slower, Not Weak

The demand environment is not collapsing, but it is clearly slowing. Clients across the US and Europe are prioritizing cost control rather than expansion. Discretionary spending, which includes digital transformation and consulting projects, has seen delays.

Even though large IT firms are reporting deal wins worth $10–12 billion in a quarter, the conversion of these deals into revenue is taking longer. This delay creates a mismatch between strong order books and near-term earnings growth. Wipro has also pointed out slower decision-making cycles, which further affects revenue visibility.

Margins Stable but Growth Missing

One of the key takeaways from Q4 is that margins remain stable even as growth slows. TCS continues to operate at industry-leading margins of around 25%, while Infosys maintains margins in the 20–22% range. HCL Tech also remains within a similar band.

However, markets reward growth more than stability. Even with healthy margins, revenue growth slowing to low single digits reduces earnings momentum. That is why stocks are correcting despite stable profitability.

Valuation Reset in Motion

The sector is now undergoing a valuation reset. Earlier, IT stocks traded at premium multiples of around 25-30 times earnings due to strong growth visibility. With growth now expected in the 3-5% range, valuations are compressing toward 18-22 times.

This compression is not a sign of weakness but a natural adjustment. When growth slows, multiples follow. The correction in stock prices reflects this re-rating rather than any major deterioration in business fundamentals. Investors are now focusing more on earnings sustainability, deal conversion, and realistic growth visibility rather than assigning premium valuations based on past performance.

Sentiment and Global Factors

Global uncertainty is also playing a role in the sell-off. IT companies depend heavily on international markets, and concerns about recession and slower tech spending are weighing on sentiment. Foreign institutional investors have been reducing exposure, which has added to the pressure.

At the same time, artificial intelligence is introducing both opportunity and disruption. While AI may drive future demand, it is also changing traditional service models. Currently, AI contributes a small portion of revenue, but it is influencing how investors view long-term growth.

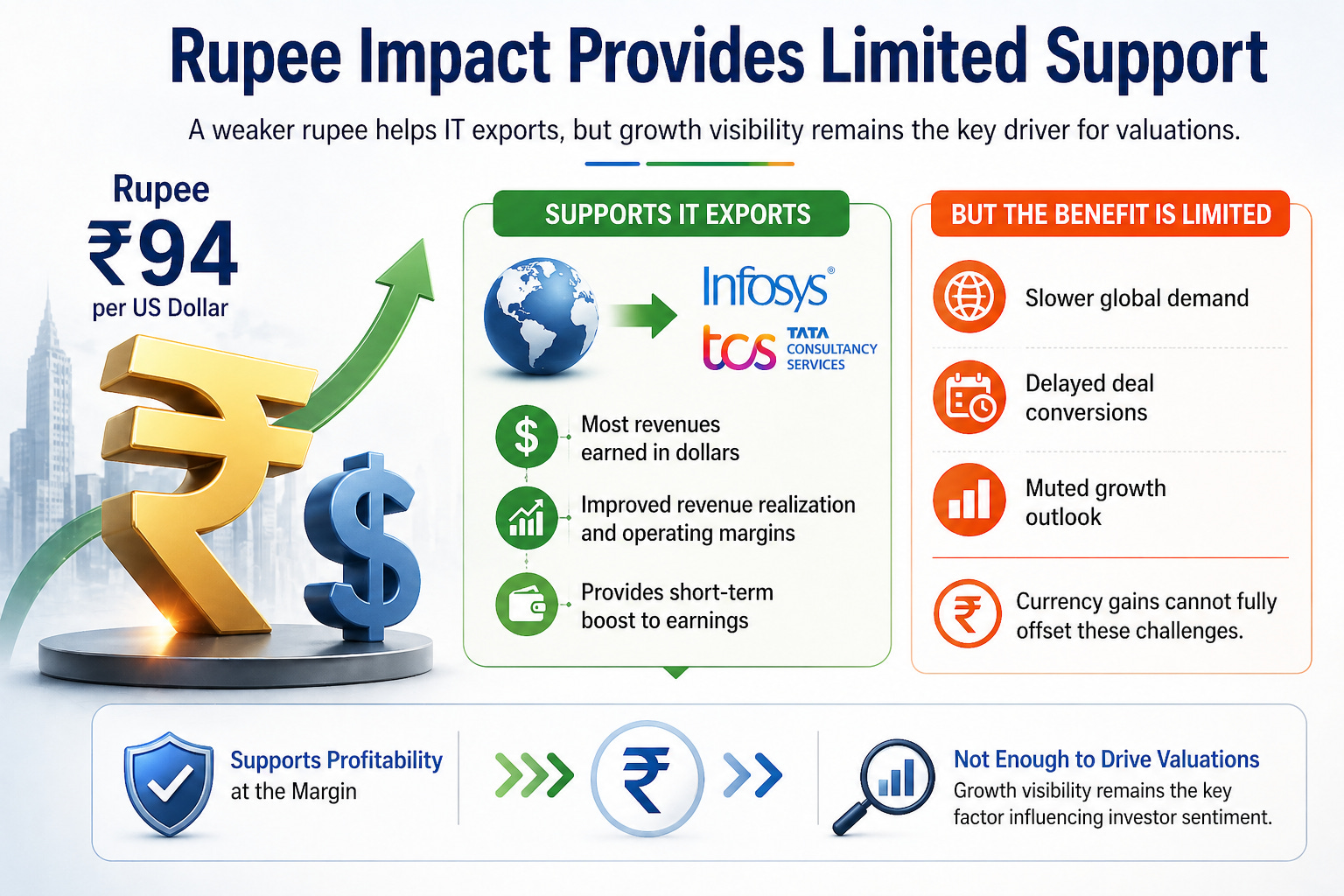

Rupee Impact Provides Limited Support

The Indian rupee is currently trading around ₹94 per US dollar, indicating continued weakness in the currency. This depreciation provides a natural advantage to export-driven IT companies like Infosys and TCS, as a large portion of their revenues is earned in dollars. A weaker rupee improves revenue realization and operating margins, offering a short-term boost to earnings.

However, this benefit remains limited and largely temporary. Currency gains cannot fully offset the impact of slower global demand, delayed deal conversions, and muted growth outlook. As a result, while rupee depreciation supports profitability at the margin, it is not sufficient to drive valuations, with growth visibility continuing to be the key factor influencing investor sentiment.

Long-Term Outlook Remains Strong

Despite the current correction, the long-term story of Indian IT remains intact. Companies like Infosys and TCS continue to have strong balance sheets, global scale, and deep client relationships.

The demand for technology services is not disappearing. It is evolving. Cloud adoption, AI integration, and digital transformation will continue to drive growth over time. The current slowdown is cyclical, not structural.

Final Takeaway

The IT sell-off is not driven by weak Q4 numbers. In fact, Q4 performance remained stable with steady revenue and profit growth across major companies. The real trigger is the sharp drop in growth expectations from double digits to low single digits.

This shift has led to a valuation reset and a correction in stock prices. While the near-term outlook remains uncertain, the sector’s core strengths remain intact. What we are seeing is not a breakdown, but a transition to a more realistic growth phase.

Lingo of the Week: Valuation Reset

Valuation reset refers to a decline in stock valuation multiples when growth expectations weaken. In the IT sector, slowing growth from double digits to low single digits has led investors to reduce premium valuations, resulting in stock price corrections.