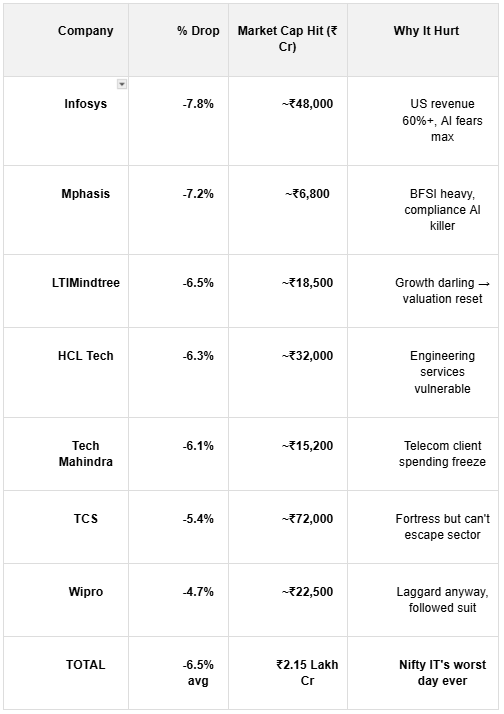

Imagine this: Monday morning, you open your portfolio app expecting the usual steady green from your IT holdings – those reliable names that have been portfolio anchors for years. Instead, you see red arrows everywhere. Infosys down 7%, LTIMindtree down 6%, TCS sliding 5%, the entire Nifty IT index plunging over 7% in a single day. ₹2 lakh crore wiped out in hours. Social media explodes with panic: “Is IT dead? Is AI eating their lunch?”

This wasn’t some random flash crash. It was a global tech selloff triggered by Anthropic’s launch of advanced AI workflow automation tools – Claude Cowork plugins that can now handle legal document review, sales analysis, compliance monitoring, and marketing workflows end-to-end. Wall Street tech giants like Salesforce and Adobe tanked 7%. Nasdaq Composite fell 1.43%. And Indian IT stocks? They got hit hardest, amplifying fears that AI isn’t just a buzzword anymore – it’s a direct competitor to the traditional IT services model.

Welcome to the IT stocks fall – not just a correction, but a market verdict on how artificial intelligence is rewriting the rules of a $250 billion industry. This newsletter breaks down what triggered this plunge, why IT stocks are uniquely vulnerable, what history tells us about such moments, and how to think about positioning through the noise.

The Golden Era That Set the Trap

For over two decades, Indian IT was the perfect growth story. Steady double-digit revenue growth. Recurring revenue from global maintenance contracts. Exposure to stable US and European markets. Margins in the mid-teens. Dividend discipline. Low debt. It was the sector you could set and forget while it quietly compounded wealth through multiple market cycles.

From post-2008 recovery through much of the 2010s, Nifty IT consistently outperformed broader markets. Even when India’s domestic growth stuttered, IT marched upward on digital transformation dollars from abroad. Valuations steadily expanded – investors happily paid 25-30x earnings for “secular growth” that seemed immune to economic cycles. Companies like Infosys, TCS, and Wipro became household names, synonymous with “safe India growth.”

But here’s what that era hid: IT’s dominance rested on a simple truth – global enterprises needed armies of engineers to maintain legacy systems, migrate to cloud, and handle complex integrations. Indian IT firms had the cost advantage, the talent pool, and the execution track record. It was a high-margin, people-intensive business model that scaled beautifully. Until AI showed up.

The Trigger: Anthropic’s AI Bombshell

February 4, 2026, will be remembered as the day markets priced in AI disruption.

Anthropic – the US AI startup behind Claude – launched workplace productivity plugins that crossed a critical line. These weren’t chatbots or simple assistants. They were end-to-end workflow automation tools capable of replacing hours of human labor across:

Legal document review and contract analysis

Sales pipeline analysis and forecasting

Compliance monitoring and regulatory reporting

Marketing campaign optimization and A/B testing

Suddenly, the market saw what analysts had whispered about for months: AI wasn’t just augmenting IT services – it was automating them entirely. Why pay millions for a team of 50 engineers to do compliance monitoring when one AI agent does it cheaper, faster, and with fewer errors?

The reaction was swift and brutal. US tech tumbled first – Nasdaq down 1.43%, Salesforce and Adobe down 7%, even AI darlings Nvidia and Microsoft down nearly 3%. Indian markets opened with Nifty IT as the biggest sectoral loser, plunging to an intraday low of 35,809.50 – its worst single-day drop in years.

Nearly ₹2 lakh crore evaporated. Even Info Edge, parent of Naukri.com, fell 6% on fears AI would disrupt white-collar hiring itself.

Why IT Stocks Are Uniquely Vulnerable

This wasn’t company-specific bad news. It was sector DNA getting exposed. Here’s why Indian IT is ground zero for AI disruption:

1. People-intensive model: 70-80% of costs are salaries. AI automation directly attacks headcount – the core profit engine. If enterprises swap 100 engineers for 10 AI agents, revenues collapse while fixed costs linger.

2. Low barriers to disruption: IT services aren’t proprietary tech. They’re execution at scale. AI can execute faster, cheaper, and 24/7. Claude Cowork doesn’t need visas, training, or appraisals.

3. Client concentration risk: North America generates 60%+ of revenues. When US CIOs see Anthropic demos, they ask: “Do we really need that $100M outsourcing contract renewed?”

4. Premium valuations: IT traded at 25x earnings during good times. When growth slows from 15% to 5%, multiples must compress sharply – from 25x to 15x is a 40% fall, even if earnings stay flat.

5. Margins under siege: Rupee depreciation helps topline but kills profitability (wages in INR). Wage inflation + pricing pressure from AI competition = double margin whammy.

The market didn’t just sell IT stocks. It priced in a business model reset.

History Says This Isn’t The End

IT corrections aren’t new. They’ve happened before – and recovered stronger.

2008-2009 Global Financial Crisis: Client spending evaporated. IT stocks fell 70-80% peak-to-trough. Recovery took 2+ years but delivered 5x returns by 2018.

2015-2016: Rupee depreciation + US slowdown crushed margins. Stocks corrected 25-35%. Multi-year consolidation led to the great 2017-2021 bull run.

2022: Post-Covid spending exhaustion + rate hikes triggered 35% Nifty IT correction. 2023-2024 recovery followed as cloud migration resumed.

Pattern: Every major IT fall followed the same script:

Overstretched valuations after multi-year runs

Client spending slowdown + margin squeeze

Panic selling (”IT is dead!”)

Bottoming: New deal pipeline emerges, margins stabilize

Recovery: Quality names lead as valuations reset

Today’s AI scare fits the pattern perfectly. The question isn’t “Will IT survive?” It’s “How fast will it adapt?”

The Adaptation Playbook Emerges

Smart IT companies aren’t panicking. They’re pivoting:

1. AI Integration: TCS launched Ignio AI platform. Infosys has EdgeVerve. HCL built ActInfinite. They’re not fighting AI – they’re selling it.

2. Higher-end consulting: LTIMindtree and Coforge focus on strategy + AI implementation, not just coding. Higher margins, stickier clients.

3. Niche specialization: Mphasis targets BFSI AI compliance. Persistent Systems does healthcare AI.

4. Cost discipline: Headcount freezes, pyramid restructuring (more juniors, fewer expensive seniors), aggressive automation of their own back-office.

The winners will be companies that sell AI services, not compete against AI tools. The market knows this – that’s why the selloff was broad-based but not indiscriminate.

How to Navigate This IT Storm

Panic feels natural. Here’s the cycle-aware playbook:

Right now (acute fear phase):

Don’t catch falling knives. Let panic flush out weak hands.

Watch weekly charts for stabilization + higher lows.

Track US tech spending surveys, AI deal pipeline mentions in earnings calls.

Bottoming signals:

Margins trough + sequential revenue growth resumes

Large deal wins announced ($100M+ TCV)

Relative strength vs Nifty 50 returns

Recovery positioning:

Quality first: TCS, Infosys (strong balance sheets, client diversity)

Growth + AI exposure: LTIMindtree, Persistent, Coforge

Avoid laggards: Weak margins, US-heavy, no AI story

Portfolio balance:

Trim IT overweight from 25-30% to 15-20%

Rotate into cyclicals (metals, industrials) leading the rally

Keep 5-10% cash for opportunistic dips

Long-term: IT at 15x FY27 earnings = compelling if they execute the pivot.

The Bigger Market Context

This IT fall isn’t isolated. It’s sector rotation in action.

Broad markets (Nifty 50, Sensex) held up better because domestic cyclicals – metals, PSU banks, infrastructure – are in a different cycle fueled by capex revival and government spending.

Money doesn’t disappear from markets. It rotates. When global tech falters, flows chase domestic growth stories. That’s healthy breadth.

Lingo of the Week: Total Contract Value (TCV)

TCV measures the total revenue from a client contract over its lifetime, not just annual billing. When IT companies start announcing $100M+ TCV deals again (especially AI-related), it’s the strongest bottoming signal. Watch earnings transcripts – “large deal pipeline” mentions spike before stocks recover.

Pocketful isn’t just another trading platform - we’re your partners on the journey to financial freedom.

Thank you for reading!

👀 Stay tuned. Stay diversified.

Until next time,

Team Pocketful.

Follow Us: Website

Download Our App: Available on Google Play & Apple App Store