Most investors have felt this before. A headline appears on the screen. It is geopolitical. It mentions ships, sanctions, or tariffs. Prices react for a day or two. Social media is filled with confident explanations. Then a few weeks pass, and portfolios look largely the same. What remains is not damage, but a quiet discomfort that is hard to measure and harder to dismiss.

This gap between noise and outcome is familiar. The headlines sound dramatic. The immediate market response feels small. Yet, over longer periods, these moments often matter far more than they seem at first glance.

Markets do not really respond to events. They respond to how power slowly reshapes incentives beneath the surface. That process is rarely clean or symmetrical. It unfolds unevenly, creates emotional confusion, and almost never comes with a clear before and after moment.

This piece looks at one such shift that is still taking shape. Oil, shipping routes, sanctions, and trade policy are beginning to intersect again in 2026. Not as separate news items, but as parts of a single developing story. A story that helps explain why many investors feel less certain today, even when prices appear calm.

To follow this story, we will rely on a simple idea that returns throughout the article. When power enters a market, prices stop being the only signal worth watching.

The Quiet Assumption Markets Like to Make

For long stretches, markets operate under a comforting assumption: that commodities are priced, goods are traded, and capital flows because incentives align peacefully enough for rules to hold. During such phases, oil is mostly oil. Shipping is mostly logistics. Trade policy is mostly negotiation.

This does not mean geopolitics disappears. It simply fades into the background. Investors focus on growth, margins, and cycles. Risk feels calculable. Volatility feels episodic rather than structural.

History suggests this assumption holds best when energy is abundant, alliances are stable, and power is uncontested enough that enforcement remains invisible. But when those conditions weaken, markets begin to relearn an older lesson: energy is not neutral, and neither are the routes it travels through.

Venezuela: Oil Without Control

Venezuela sits at the heart of this story not because it is powerful, but because it is resource-rich without control. It holds the world’s largest proven oil reserves, yet for years has struggled to convert that geological wealth into economic stability. Sanctions, institutional decay, and political isolation turned oil from a blessing into a bargaining chip.

For the United States, Venezuela has long represented a contradiction. A nearby energy giant, politically hostile, economically weakened, and increasingly aligned with rival powers like China and Russia.

When global energy supplies were comfortable, this tension could be handled with time and pressure. Sanctions, diplomacy, and economic limits were often enough. As supply became tighter and global politics grew more divided, waiting became costly. That change is important. When energy becomes scarce, the boundary between economic pressure and physical action starts to fade.

Recent actions in Venezuela point to this shift. What was once controlled mainly through financial restrictions has moved toward more direct intervention. Reports of significant loss of life show that the situation has crossed into a different phase. The issue is no longer just about enforcing rules or compliance. It is about control over resources becoming open and visible, rather than indirect or implied.

From Sanctions to Seizures: A Subtle Escalation

Sanctions are usually spoken about as financial tools. In reality, they work through logistics. A barrel of oil under sanctions is not only a legal issue. It becomes a problem for shipping, for insurance, for routing, and for finding willing buyers and sellers. As enforcement becomes stricter, the focus shifts. Attention moves away from balance sheets and contracts toward ships, sea routes.

Recent actions by the United States involving the seizure of oil tankers linked to Venezuela reflect this change. Some of these vessels were operating under foreign flags. Officially, these steps are presented as law enforcement actions meant to uphold sanctions, prevent illegal trade, and protect international norms.

From a narrow legal view, this explanation is internally consistent. From a market view, something broader is unfolding. The reach of enforcement is moving outward, from banks and transactions to oceans and vessels. When this happens, markets receive a different signal. It is no longer only about how much supply exists, but about who is willing to enforce rules physically, and where that enforcement is likely to occur.

Enforcement Replaces Neutrality in Global Trade

The seizure of the Russian flagged tanker Marinera, formerly Bella 1, marks a further escalation in sanctions enforcement. Intercepted in international waters for allegedly transporting Venezuelan oil, the vessel had reportedly changed its name and flag to evade detection.

Moscow views this seizure as a violation of maritime norms rather than routine policing. This incident reinforces the reality that shipping tied to sanctioned energy is now vulnerable to physical seizure.

For the global trade community, the message is clear: participating in these routes involves physical and legal risks that transcend simple contract agreements.

International waters are only neutral when global powers agree on the rules. As that consensus weakens, enforcement becomes a strategic tool. This transition makes global commerce less predictable, placing a heavy burden on import dependent nations that rely on stable maritime corridors to maintain their energy security and economic health.

The shipping industry is already adapting to this new friction. Insurance premiums are climbing, delivery routes are lengthening to avoid high risk zones, and compliance costs are surging. Companies must now navigate a complex web of overlapping rules, making every shipment a potential legal and financial liability.

While individual delays may not cause immediate panic, their cumulative effect is substantial. These constant frictions force businesses to reassess the long term viability of certain trade relationships. What started as targeted legal enforcement is slowly but fundamentally reshaping how global trade operates on a daily basis.

Ultimately, logistical reliability and risk management are becoming as vital as price. Markets are discovering that as geopolitical power extends into trade routes, true neutrality disappears. In this environment, the ability to safely move goods through contested waters is becoming the most critical factor in global economics.

Energy as Leverage, Not Just Supply

Recent events with Venezuela and Russia are not isolated incidents but part of a historical pattern. When global power is challenged, energy stops being a simple commodity and becomes a tool for political pressure. Powerful nations use oil to send quiet messages of control, making the global market feel less stable.

This environment is particularly difficult for countries like India. Energy is no longer just a background cost; it is now a strategic lever used in diplomacy. As trade routes become less predictable and risks rise, India must navigate a world where fuel security is tied to shifting alliances and international power struggles.

India’s Position: Practical, Not Ideological

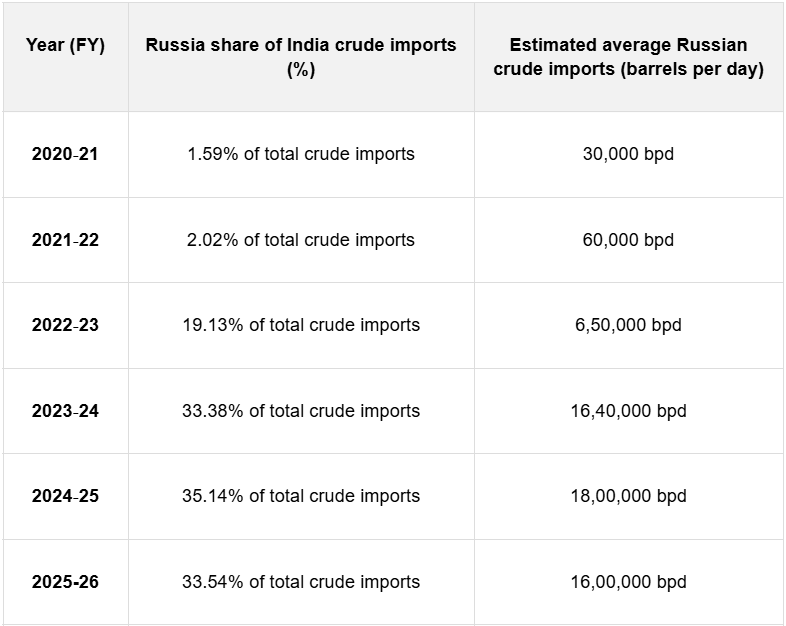

India’s engagement with sanctioned oil flows has been driven more by arithmetic than ideology. During periods of global energy stress, discounted crude offered a way to control inflation, protect the current account, and cushion domestic consumers. Whether the source was Russia in recent years or Venezuela earlier, the underlying logic remained consistent. Economic stability took precedence when traditional suppliers became expensive or unreliable.

This approach reflects India’s long standing policy of strategic autonomy. Energy decisions have typically been framed around resilience rather than alignment. For markets, the immediate impact was stabilising. Lower input costs eased near term pressure at moments when global volatility limited alternatives.

What changes across cycles is not intent, but context. In both cases, India’s initial response was shaped by opportunity created by disruption elsewhere. Dislocations in global supply opened space for pragmatic choices that made economic sense at the time.

Over time, however, enforcement tightened around shipping, insurance, and trade routes. Political risk gradually entered what began as a purely economic calculation. Supplies did not stop abruptly. Instead, uncertainty crept in, complicating procurement, compliance, and long term planning. Import patterns from both Russia and Venezuela reflect this shift from accessibility to conditionality.

India now faces a recurring tension rather than a one off challenge. Affordable energy security must be balanced against access to major export markets and stable trade relationships. Many mid-sized economies face similar trade-offs, but India’s scale makes this balance more visible. The task ahead is navigating an environment where economic logic increasingly operates within political boundaries.

The Tariff Threat: When Trade Becomes a Signal

Threats of tariffs as high as 500% from the US on India for buying Russian crude oil are signals rather than real plans. These extreme numbers aim to grab attention and set boundaries. This reminds partners that access to major consumer markets is a strategic privilege and not a guaranteed right.

For India, the impact depends on specific rules. This is why markets often stay calm. The deeper concern is the precedent being set where energy choices are directly linked to trade punishments.

This linkage creates long term uncertainty. Companies struggle to plan expansions when market access feels tied to shifting foreign policy. Investors cannot easily predict profits when trade stability depends on politics instead of business fundamentals.

Geopolitical pressure creates financial stress by eroding confidence. The mere threat of unpredictable trade barriers can stall investment and cloud the economic outlook for years.

How Markets Process Political Pressure

Markets are not moral actors. They are adaptive systems. When political pressure enters the economic landscape, markets rarely react with a single dramatic move. Adjustment happens gradually. Exporters reassess exposure, supply chains look for backup options, capital demands higher safety margins, and currencies begin to absorb subtle risk premiums. These changes do not signal panic. They reflect slow adaptation.

This is why markets can appear calm even as underlying stress increases. Visible reactions often fade quickly, creating the impression that little has changed. But adaptation works quietly. It reshapes decisions inside companies in ways that do not reverse just because headlines disappear.

A supply chain manager diversifying production locations is responding to long term uncertainty, not daily price swings. A corporate treasurer adding layers to currency hedging is acknowledging that political risk has become real and persistent. These choices last far longer than the news that triggered them.

For companies, this environment creates stress without necessarily leading to collapse. Export oriented firms dependent on specific markets feel policy risk more acutely as access conditions become less predictable. Energy intensive businesses may benefit from lower costs but remain exposed to shifting routes, insurance limits, and compliance burdens.

For investors, this phase is less about identifying clear winners and losers. It is about understanding how confidence changes across cycles. In stable periods, confidence is expansive. In transitional periods, it becomes cautious and defensive. Business models built for continuity struggle, while those designed for flexibility gain value in uncertain conditions.

The Pattern Repeating, Not Escalating

It is tempting to view current tensions as steps toward inevitable conflict or systemic breakdown. However, history suggests caution. Great power systems often experience long periods of friction, trade threats, and symbolic confrontations without ever tipping into direct war or total economic separation.

What changes is not necessarily the endpoint, but the texture of risk. History offers various models: the Cold War’s sustained growth despite proxy conflicts, the interwar period’s rapid fragmentation, or the post Napoleonic century’s series of limited transitions. Multiple patterns exist beyond a linear path to catastrophe.

In these transitional phases, markets shift their priorities. They begin to reward resilience over optimization, flexibility over efficiency, and careful balance over strong conviction. This is a recurring behavioral observation rather than a specific forecast.

Recognizing these historical patterns helps us navigate the present. Understanding that friction is a common feature of global systems allows businesses and nations to plan for a future defined by complexity rather than simple collapse.

A World of Friction, Not Free Flow

What emerges from this story is not a sense of imminent collapse, but a steady rise in friction. Oil continues to flow, trade continues, and markets still function. The difference is that each now operates with more conditions attached, making the system feel heavier and less fluid than before.

When power enters energy markets, neutrality begins to fade. As enforcement moves beyond legal frameworks into physical intervention, predictability shrinks. Trade increasingly signals alignment rather than serving as a purely economic exchange, and business decisions grow more complex as a result.

Investors often sense this shift before they can clearly explain it. Portfolios may remain intact, yet confidence feels less secure. Valuation narratives that once felt complete begin to show gaps. That discomfort is not noise. It is information that deserves attention.

Friction rarely arrives with drama. It builds through small, reasonable changes such as higher insurance costs, longer routes, and heavier compliance. Each is manageable on its own. Together, they reshape which business models endure. This is not a moment for panic, but for recalibration and thoughtful adaptation.

The Carry Forward Lens

What should a reader take away from all this is not a position on Venezuela, not an opinion on tariffs, and not a market forecast. What matters instead is a way of seeing how markets behave when power becomes more visible.

In such phases, prices tend to react late. Behavior moves first. The earliest signals do not appear in valuations, but in quiet adjustments. Companies hedge before they explain. Trade routes change before prices reflect the shift. Confidence redistributes well before capital flows make it obvious.

Cycles rarely announce themselves clearly. They surface through incentives changing beneath the surface. A shipping company choosing longer routes to avoid certain waters reveals more about perceived risk than any official statement. An exporter accepting higher costs to diversify markets reflects a reassessment of concentration risk. Capital favoring firms with geographic balance over pure efficiency signals a repricing of resilience.

Paying attention to these behaviors has a stabilizing effect. It replaces the urge to react to headlines with the clarity that comes from recognizing patterns. In markets shaped as much by power as by price, calm is not detachment. It is understanding.

What Comes Next

What comes next is still unresolved. India has neither fully aligned with US energy expectations nor openly resisted them. Private refiners have shown some flexibility, while state buyers continue to follow economic logic. Enforcement has tightened, but it has stopped short of direct action against Indian oil companies or financial institutions. This is not a resolution, it is managed tension.

What is clear is that the old rules are weakening while new ones are still taking shape. Energy security, trade flows, and shipping are no longer neutral background systems. They are increasingly shaped by power, signaling, and enforcement. Companies and countries are adjusting as they go, rather than following a stable rulebook.

Recent market volatility should be read in that context. Not as panic, but as recalibration. A slow repricing toward a world where geopolitics matters more and economic logic operates within tighter limits.

For investors, the task is not to predict outcomes, but to recognize transition. Periods like this reward clarity over conviction and adaptability over attachment. The real question is whether one is paying attention to the behaviors that show what is replacing the old order.

Lingo of the Week: Geopolitical Pricing

Geopolitical Pricing refers to the way financial markets incorporate political relationships, sanctions risk, trade tensions, and strategic alliances into asset prices. Valuations shift not only on profits or growth, but also on diplomatic signals, policy threats, and changes in global power dynamics.

Pocketful isn’t just another trading platform - we’re your partners on the journey to financial freedom.

Thank you for reading!

👀 Stay tuned. Stay diversified.

Until next time,

Team Pocketful.

Follow Us: Website

Download Our App: Available on Google Play & Apple App Store